INDEX 3

25 April–1 May, 2026

It’s been a surprisingly warm week in London – clear skies and rising temperatures, all leading up to the start of an early British summer this Friday on May Day. I had the pleasure of watching local men prance about in foliage around my town to enact a Victorian Jack-in-the-Green revival, and to later hear a talk from RMT boss Eddie Dempsey in commemoration of International Workers Day. Dempsey spoke to the argument that trade union power ought to come before political expression, to which I wholeheartedly agree. If workers seek to change the world in favour of labour interests, then unions need to take the lead and put aside petty sectarianism in favour of maximising the total strike power of the class (editor’s note: if this point annoys you, read here).

I have also been watching this week with interest the fallout of Your Party’s dismal failure, as the embers of the movement seek to recoup and reassess their standing in the aftermath. Whilst large sections of the rank-and-file have either reverted to their home socialist groups or have joined to the ascendant Green Party, some – such as the author of State & Confusion – have sought to provide a more rigorous political analysis, in what seems like an earnest endeavour to build from past mistakes. What is to come from this is yet to be seen, though I hope the more fragile material circumstances become, the more the RMT’s efforts to expand overall strike power and build broader organised labour fraternity will manifest in more compelling and resilient political experiments.

This week has seen the ramping up of competition and insecurity in global energy markets, as the AI sector faces its first major market wobble and the UK prepares to go to the polls on politically meaningful but materially meaningless terms. Mao-era national planning organisations at the heart of Chinese government are rapidly matching the investment capacity of entire Western stock exchanges in order to accomplish feats of engineering deemed impossible for any country only a few years ago, whilst US infrastructure is struggling to match the requirements needed for the country’s last-ditch bid for dominance in the AI sector. The patheticism of the moment is rather well captured by the malaise of British politics, where right- and left-wing pretenders are closing in on a political establishment steadfast in its refusal to embark on state capacity expansion, all in the name of keeping the peace with bond markets one might very well expect to see collapse into an artificial chaos in the coming months. With the UAE ending its longstanding membership of OPEC, and no end in sight for the blockade over the Strait of Hormuz, workers in the West should be asking themselves the same questions regarding what relevance the existing form of party politics has for the emerging global conditions.

— S.E.P.

‘Bragawatts’

A new white paper from the Oxford Smith School and Marex reveals a significant delivery gap in AI infrastructure, suggesting that 35-50% of planned AI data centres are behind schedule. The report claims several contributing factors, including what the authors refer to as ‘bragawatts’: commodities like copper and electrical steel priced on the basis of announcement curves (buildout claims) rather than actual delivery, causing short-term overpricing followed by oversupply and market crashes.

Delivery has also been impacted by energy demands, with national grids not developing rapidly enough to meet the demands of larger AI data centres. This Thursday, the UK National Grid produced a request for all new AI developments – now heavily encouraged by the government’s ‘Sovereign AI’ scheme – to set up base in Scotland, as the English grid cannot handle the projected burden. This has also encouraged the development of off-grid solutions in energy production such as natural gas turbines and fuel cells, expected to contribute to higher electricity prices, gas prices, and delayed fulfilment on Net Zero goals. Regardless of the concerns, however, energy facilitation is not meeting demand, causing serious worries about long-term sustainability not just for the energy market, but for AI RoI.

On Tuesday OpenAI revealed it had missed several key performance targets, causing share prices to fall sharply. SoftBank stocks dropped as much as 9.9% in Tokyo, whilst infrastructure and cloud providers Oracle and CoreWeave dropped 5% and 6.2%, respectively. Semiconductor chip makers also saw a decline of roughly 4%, compounding fears around a potential bubble-burst as a result of AI over-speculation.

The overall picture is that of speculative over-ambition, and the limitations of physical reality. Credit exists as an exercise in imagination, positive assertions about potential profitability in the short-to-medium term. This leaves it physically divorced from the material circumstances on which those predictions are built. That we can see AI models developing and interact with them in the imaginary is more important for market growth than the hard requirements of infrastructural resourcing. Of course, data clouds are physical and not metaphysical entities; Hyperscalers can only do so much, particularly in an America which has taken great pains over the course of the last few years to severely hamper its resourcing capabilities through trade wars and geopolitical grandstanding, on top of stagnation in the labour market matching none of the employment boosts expected by deportations and public sector trim-downs.

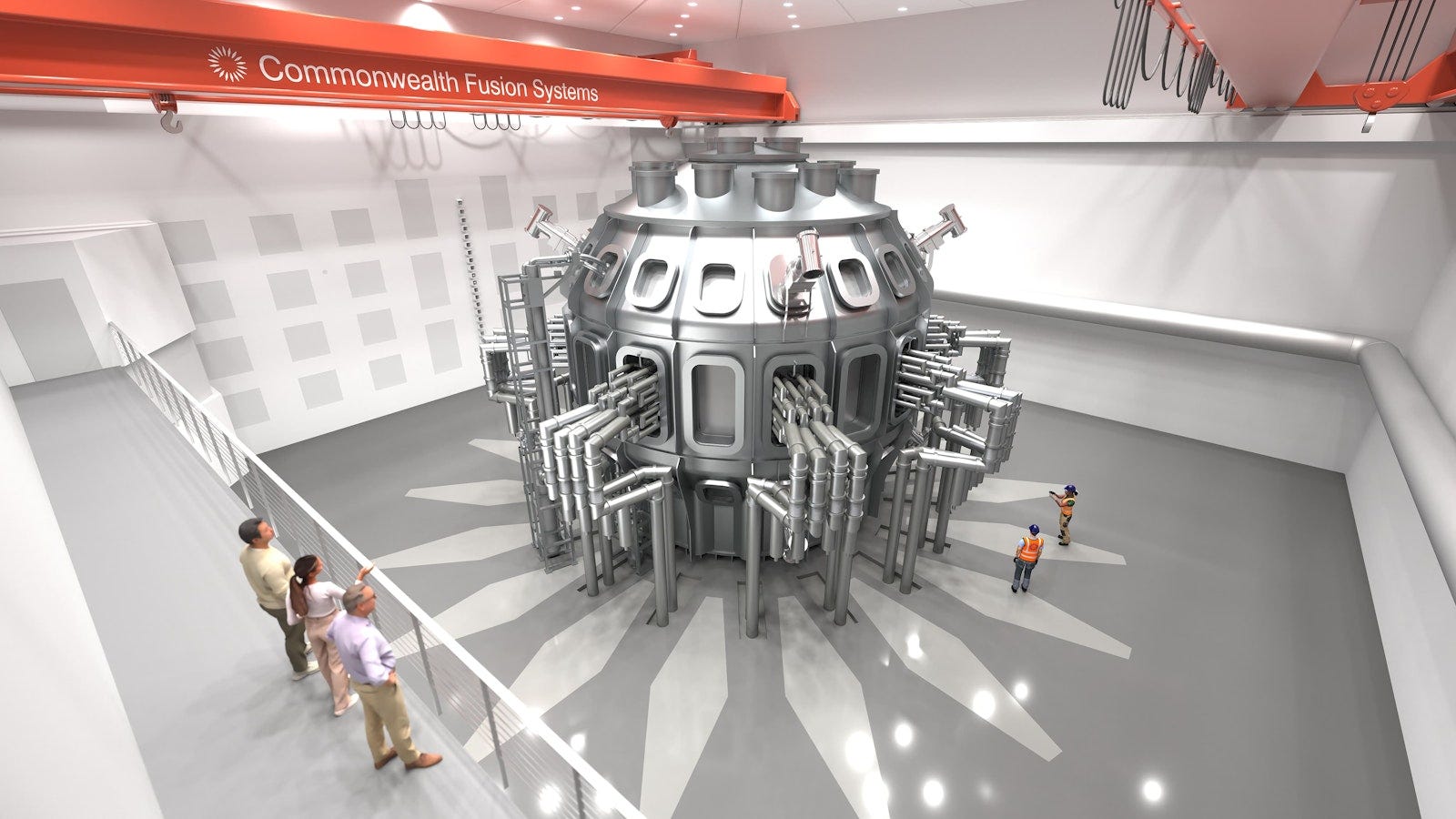

State Fusion vs. Venture Capital Fusion

The race for fusion-based nuclear energy continues as Western governments continue their desperate search for locally-sourced and dependable large-scale energy supply. This week, Commonwealth Fusion Systems, one of America’s leading fusion research groups, declared its expectation to reach capacity for grid supply within the early 2030s. This marks the first large-scale supply target worldwide for fusion technology, competing with the expectations set last week by OpenAI spinoff Helion to supply fusion energy to Microsoft by 2028. Of contrast here, however, is a promise to provide grid-scale solutions, potentially offering far greater gains for nationwide energy security than the modular reactors promised by Helion.

Successfully reaching this target would be a tremendous boon to US energy security, as fusion technology remains a mainstay of US research departments. The Chinese Fusion Energy Company (CFEC), a state-led venture backed by the Chinese National Nuclear Corporation, is rapidly catching up with US projects, as the PRC wields its immense state investment tools to match 8 years’ CFS investment in 1 year. CFEC aims to have its fusion reactors supplying grid power by 2035, and is actively seeking to be the first reactor to do so, marking both a geo-strategic and political race for the claim to the world’s first grid-supply fusion power.

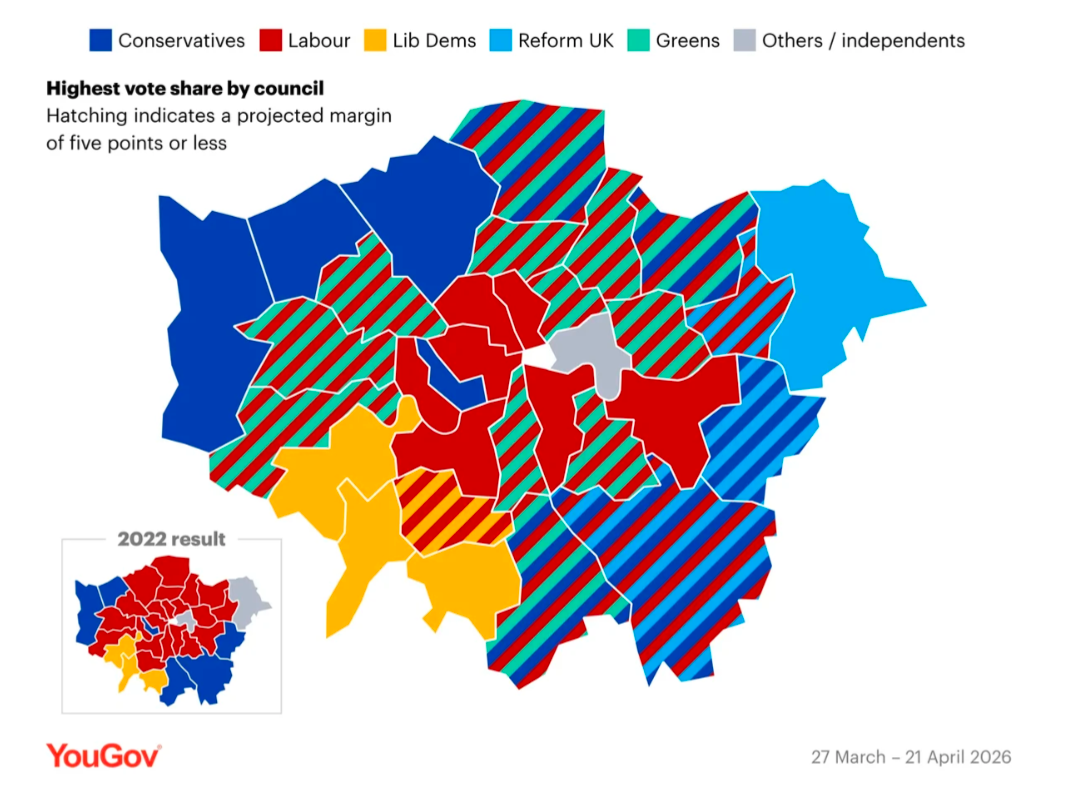

UK Local Elections

The British public will go to the polls this Thursday in a string of local and devolved government elections that will likely turn out the most politically upsetting results some areas have seen in decades. Polls have consistently demonstrated a disastrous outcome awaiting the governing Labour Party, as Reform UK and the Green Party hope to take control of several Labour heartland councils, including areas which have been led by Labour councils for over a century. Nationalist parties SNP and Plaid Cymru are also expected to perform well in Scotland and Wales, respectively, as a short-lived Labour revival comes crashing down into the latest existential crisis for the British union.

Mainstream electoral politics in the UK has been struggling to maintain its footing ever since 2014 when the question of Scottish independence was put to referendum, followed by the victory of the Vote Leave movement during the Brexit referendum in 2016. The properties of a first-past-the-post system in which voters are encouraged to hedge in order to achieve governmental results has thus far been enough to keep the mainstream parties stable, even as both the Conservative and Labour parties experienced populist turns in the run-up to the COVID-19 pandemic. A string of political disasters coupled with a loss of political appetite for populism saw the newly centralised Labour Party assume power at the 2024 general election for the first time since 2010, but in the years since populism has reasserted itself.

Whilst local elections can serve as good indicators on popular sentiment at the halfway point of a government tenure, the outcomes are less than decisive; municipalities across England are overstretched to the point of no return, with a growing number forced to issue Section 114s (effective bankruptcy notices) as central government funding legally required for the operation of these municipalities dries up under a regime of fiscal conservatism intended to satisfy bond markets. This leaves the vast majority of would-be councillors with very little tangible goals to offer the electorate, besides aiding in a party-building exercise with national governing ambitions. Nonetheless, Reform UK and the Greens are making incredible promises in order to secure local votes, knowing full well the limitations of their potential office.

The story is similar in Scotland and Wales where, despite some degree of political devolution, national governments are largely constrained by fiscal regulations and national policies. Wales in particular has long been controlled by the Labour Party, which looks to be facing a major political overturn as part of a revolt against Keir Starmer’s Westminster government, in favour of Plaid Cymru. Certainly the last thing the British government needs is yet another national cessation movement, yet the age is demanding political restructuring on a tremendous scale. The question then becomes as to whether unionists, either right or left, can properly articulate what a renewed British union might look like, given that everyone is in agreement that the present settlement is losing the last of its inertial legitimacy. What neither side can say with any degree of certainty is what effect a major restructuring will have for material economic growth; in any case, the situation would not appear optimistic.

UAE Leaves OPEC

The United Arab Emirates officially ended its involvement in OPEC this Thursday, in response to increasing instability on the global oil market led principally by the US-Israeli war on Iran. At its foundation in the 1960s, OPEC was intended as a bid to shore up sovereign oil interests against private prospectors by agreeing on joint production limits in order to control global prices, established concurrently with other inter-sovereigntist bodies such as the Non-Aligned Movement. Decades since its foundation OPEC has seen its overall market share and price-setting powers diminish drastically, with the US-Israeli war on Iran sending prices skyrocketing despite OPEC interventions. The UAE, described as the ‘naughty boy’ of the group in a now deleted tweet by a Saudi official, has often flouted the production limits agreed upon by the group, however its departure this week signals a significant shift in policy toward ramping up production in order to capitalise on market shortages and accelerate global competition on output. Some have suggested that the departure marks the beginning of the end to the group, however Saudi officials have asserted that they are unperturbed by the developments.

The Atlantic Council’s Global Energy Agenda 2026 report, published this week, stated that half or more of energy observers saw geopolitical rivalry as the greatest threat to energy security in the run-up to 2030, largely due to infrastructure requirements rather than outright conflict. As governments turn funding away from critical capacity development and towards arms manufacturing and defensive operations, long-term delivery capacity on energy targets lags or reverses, particularly with energy-intensive markets such as AI and space travel puting immense pressure on existing national grids.

The Atlantic Council also noted that China has positioned itself as the ‘dominant architect’ of energy capacity in the Global South, with investments in developing countries’ energy infrastructure rapidly outpacing US and Western infrastructure investments, establishing long-term energy dependence on Chinese parts. The Chinese have also firmly established their dominance in the renewables market, as Western countries like the UK and France seek to transition away from volatile fossil fuels toward more ‘sovereign’ green energy infrastructure.

Developments in energy markets are pointing towards the collapse of the post-war petrodollar world system and of some kind of cleavage between the interests of global capital on the one hand, and the requirements of growing geopolitical instability on the other. As bodies like OPEC and hegemonies such as the US’ start to collapse, the only apparent winner from the chaos is, at least for the time being and for some time to come, the People’s Republic of China.

INDEX Verdict

Global energy markets are in turmoil, speculative AI bubbles are expected to burst soon. Workers should be seeking to build anti-sectarian union-based alliances for the sake of effective strike action in order to push Western economies out of financialisation and toward state-led development, ignoring largely meaningless electoral contests.