INDEX 1

13–17 April, 2026

Monday 13 – Friday 17 April, 2026

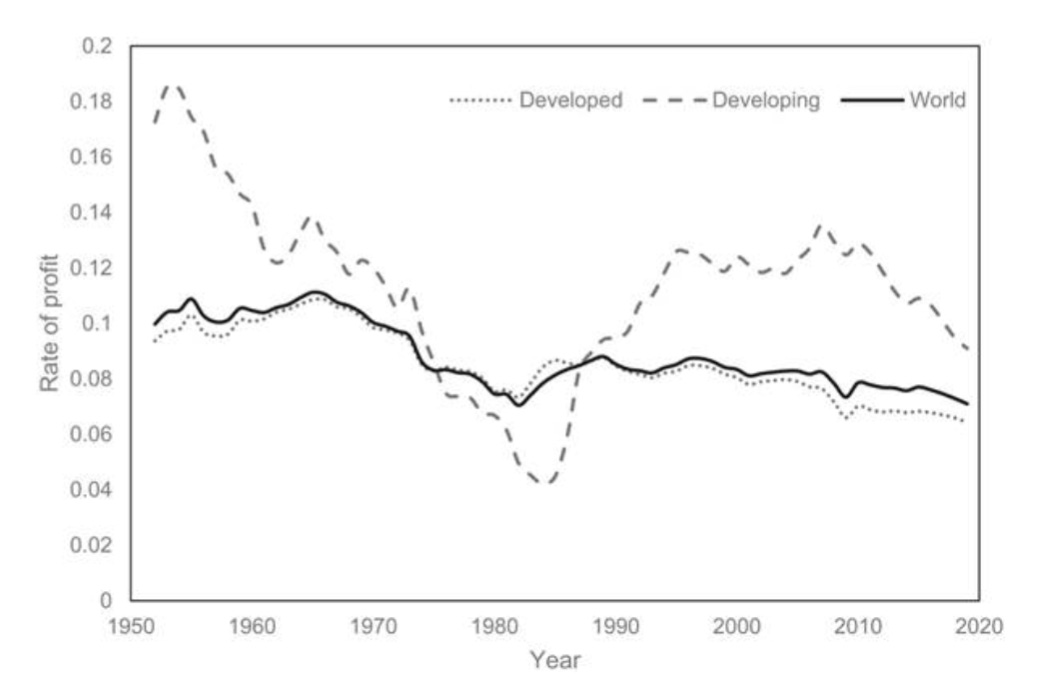

Global profit rates are in terminal decline, a reality confirmed by new data from Sydney University. Post-pandemic recovery has flatlined into a downward trend in surplus value,

Current hyperscaling is a capital trap. Up to 80 per cent of AI CapEx is tied to depreciative hardware maintenance (C/V) with negligible productivity yields.

Miliband commits to Small Modular Reactors (SMR) which facilitate a fragmented, high-maintenance energy regime designed to appease credit markets.

IEA declares Hormuz closure the ‘greatest disruption in history’, as Iran agrees to reopen the strait [then closes it again].

Recent 93% Ofgem strike mandate signals the seizure of the state's regulatory centre, precisely as it attempts to license a new nuclear future.

The landslide victory for Péter Magyar (138 seats) signals a debt-for-compliance swap intended to unlock €20bn in frozen EU credit at the cost of Hungarian sovereignty.

The New Physiocrats

Can Miliband’s Electrostate Work?

New data from Sydney University confirms that the post-2008 credit regime - conceived as an administrative guardrail - is hitting a thermodynamic wall. We are witnessing the exhaustion of profitability; the state is no longer cooling market pressures but attempting to floor-plan a reality where profit has ceased to be the primary engine of growth (see ‘On Credit’, LL 07/04/26). This is not to say that profit has disappeared entirely, but global economies are adjusting to an uncertain future accordingly.

A recent New Statesman profile from Will Lloyd confirms that Ed Miliband is in regular contact with economist Adam Tooze, and that Miliband’s intellectual allies describe America under Trump as “aligning itself with the petrostates,” as well as calling Nigel Farage a “Fifth Column” for America’s petroleum interests. The framing of an economic world conflict between petrostates and electrostates is directly taken from Tooze, used by Miliband’s circle as the conceptual vocabulary for understanding our present geopolitical moment. Ultimately the electrostate is – besides its environmentalist exterior – a means to reground domestic energy product in a more qualitatively sovereign and resilient material foundation, moving beyond the post-Bretton Woods petrodollar regime towards a more multilateral geopolitical-economic order.

Meanwhile, the efficacy of these developments in Britain seem to be slow going, with the ancillary logic of the petrodollar regime covertly shaping the nature of our ‘electrostate’ in construction. In the UK, Net Zero targets have developed a further iteration of rentierism. Miliband’s Clean Power 2030 is not primarily a decarbonisation strategy, nor primarily an energy security strategy, though it presents itself as both. Rather than climate sovereignty, the project serves more so to escape terminal industrial declines through the state-directed constitution of a new generation of underlying assets adequate to underpin the next cycle of credit expansion. Inverting 1990s state-led growth theories, the government has moved from being a catalyst for private expansion to being a nationaliser of the cost of the present.

Critics to Miliband’s right often compare CP30 to Chinese policy towards their own electrostate transition. China’s advanced integration of state planning, manufacturing scale, and technological development – irreducible to renewable infrastructure alone – make them the world’s archetypal electrostate, and therefore the only realistic available model for a figure like Miliband to emulate. China’s photovoltaic production capacity is now 4.5 times the entire rest of the world combined, despite immense Western efforts to compete between 2022 and 2024; what China demonstrates is that the degree to which a country is (or can be) an electrostate comes down to what level of economic and governmental rationality the state can deploy, as well as capacity to absorb the shocks of global energy supply crises without destabilising the institutions of the state.

The form of sovereign economy Miliband is attempting to construct represents a retreat to the natural monopoly of energy now that the frontier of industrial profit has closed. Treasury political economy appears to have regressed to a pre-industrial synthesis to address a post-industrial reality, the fundamental problem of profitability being too large an object to seriously address. In the 1700s the Physiocrats observed that the wealthy derived their produit net, or surplus, from control of the natural bounties of agriculture. In our period, the manner by which the treasury views energy demonstrates an equivalence with the formal properties of cyclical regularity and predictability that agriculture formerly held for the political economy of the 18th Century – albeit refracted through the logic of high finance.

Contracts for Difference (CfD) agreement guarantees a renewable energy generator a fixed strike price for electricity over twenty years regardless of market fluctuations, meaning a future income stream is capitalised at a discount rate to produce a present asset value which can serve as collateral for the state. The state, through the CfD, massages a baseline of predictability which serves as the material basis for the sustenance of the credit system – the bottom line is that even if Miliband wants to pursue the electrostate model to emulate China’s sovereign resilience, he would be unable to do so without also ending the present system of administered credit. The Chinese government is able to pursue the electrostate model to a profound level of efficacy due primarily to their infrastructure-led developmental model, wherein neither profit nor debt factor as decisive constraints to further development, whereas in Britain profit remains a reified signal determining creditworthiness. Unless that system is overturned, no amount of effort on Ed Miliband’s part will build lasting sovereignty in Britain.

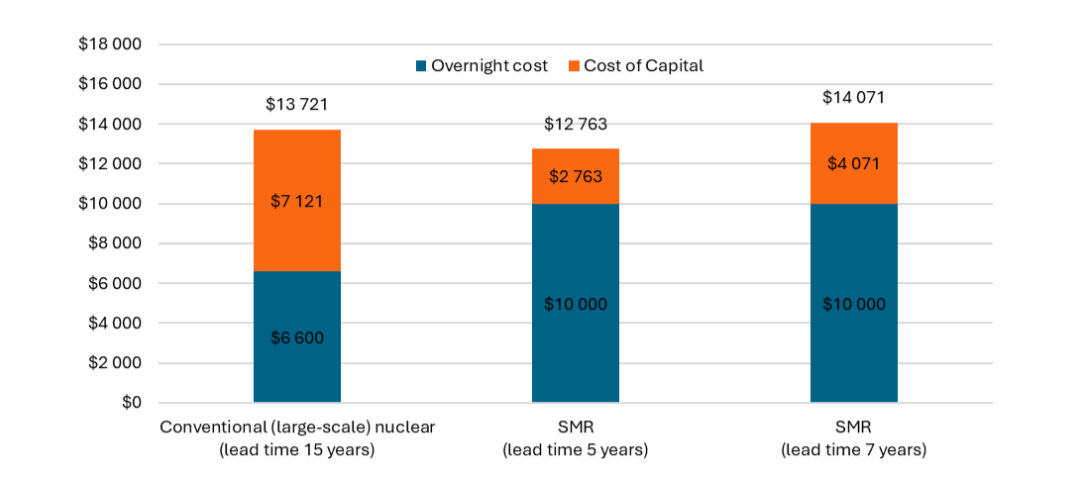

The recent contract between Great British Energy - Nuclear (GBE-N) and Rolls-Royce SMR to deliver three Small Modular Reactor (SMR) units at Wylfa – backed by a £599mn National Wealth Fund facility – is a clear demonstration of treasury orthodoxy at work. By opting for modular units over large-scale, centralised gigawatt plants, the state avoids the transformative investment required for genuine long-term security. Instead, it introduces a fragmented energy regime of shorter-lived, depreciative hardware assets. These units require constant maintenance and are distributed only to firms with significant disposable credit, reinforcing the artificially 'competitive' energy markets that the green turn was meant to overcome.

A key argument made for SMRs center on energy queues. Industrial investment efforts are currently held back by carbon regulations and grid connection queues of up to 10 years; SMRs supposedly provide a rapid, government-sponsored bypass to wait-times for National Grid connection. The reality is, however, that SMR regulations are far denser than carbon regulations, requiring geological and radiological groundwork that puts industrialists in the position of nuclear operators. Despite government subsidies and the £2.6bn allocated in the 2025 Spending Review, SMRs remain more expensive than traditional grid solutions with higher long-term overheads. This strategy may appear impressive to speculators, but the fact is the UK government is downsizing national energy capacity to appease bondholders, pricing in permanent energy scarcity to maintain short-cycle assets and bond liquidity.

INDUSTRY

Sovereign AI and Virtual Unemployment

American capital is gambling its remaining surplus on an AI ‘miracle’, with investment hitting a record-breaking $2.25trn worldwide as of 2026. Yet up to 80 per cent of expenditure is still being burnt on maintaining hardware that offers zero productivity in physical supply chains. This fuels a post-industrial unemployment trap, where displaced labour is absorbed into socially unnecessary work to justify consumption, further draining the net social surplus.

The UK is applying the same physiocratic logic to its own burgeoning AI market. Science Secretary Liz Kendall’s ‘Sovereign AI’ – a £500mn state-backed venture facility announced on Thursday - intends to utilise the state’s monopoly on computing power to anchor developers to the national growth agenda. But ‘AI sovereignty’ is a lagging indicator. As the IMF slashes UK growth expectations further than any G7 peer this week, Britain is merely jumping onto a pilgrim’s bandwagon just as the global surplus that funded it begins to evaporate.

LOGISTICS

“The Largest Energy Supply Disruption in History”

Friday saw the end to what the International Energy Agency (IEA) officially declared the largest oil supply disruption in history, exceeding the 1970s crisis; Saturday saw it potentially begin again.

From the start of the closure to Friday 17 April, this has amounted to a 10.1mn barrel per day decline in global supply, with wholesale gas prices jumping 75% since 28 February. Brent crude this month sat at $112 before Tehran and Washington came to their brief agreement to keep the waterway open prompted by of the 10-day ceasefire between Israel and Lebanon.

The UK is projected to have lost about 440mn barrels in supply for April alone, with European stockpiles notoriously unprepared for a crisis of this magnitude, and putting extreme pressure on EU commitments to continued sanctions on Russian energy imports. Reeves’ securonomics agenda is being pushed to its limit by an increasingly unstable global economy.

LABOUR

Red Tape on the Picket Line

On Monday, PCS members at Ofgem renewed their strike mandate with a 93 per cent 'Yes' vote. This follows from strike action taken in mid-2025 over pay security against inflation, which saw workers undertake targeted paralysis action to severely frustrate the regulator's agendas.

Last year's strikes were targeted to hit offices during the quarterly gas price cap announcement, causing significant delays to publication for key documents related to energy policy and leading to a data fog in the market. They also successfully increased union density at Ofgem by 150 members in a single month, leading to this week's mandate increase of 7.77 percentage points, a number high enough to give the union the power for a 10-day notice ‘lightning strike.’

This comes at a particularly vulnerable time for Miliband’s DESNZ as lengthy paperwork awaits the implementation of new SMR contracts and market frameworks for the UKAEA fusion roadmap, both announced this week, on top of increasingly volatile oil prices that require hair-trigger government responses to protect industry and consumers.

Emboldened by the Employment Rights Act 2025, which allowed the extension of strike mandates to 12 months and removed minimum service requirements, the nature of the government’s social-democratic-degrowth efforts remain evidently paradoxical and unresolved.

GEOPOLITICS

The Fall of Actually-Existing Postliberalism

Sunday's Hungarian election results brought back a landslide victory for Peter Magyar, winning a two-thirds supermajority at 77.8 per cent turnout. As JD Vance's desperate attempt to campaign for the outgoing Prime Minister during his visit to the country demonstrated, this victory points to something of a formal closure of the illiberal moment in Europe.

Orban's Fidesz has long played the thorn in Europe's side, vetoing several large-scale funding initiatives for Ukraine in its war with Russia, and playing both Russia and the EU off one another, a strategic posture which a large section of the western right – including in the Trump administration – regarded as a pragmatic, ‘postliberal’ formula for geopolitical engagement. This strategy has not been paying any dividends in recent years, however, with average wages in Hungary the third-lowest in the EU and prices suffering the highest levels of inflation post-COVID in Eastern Europe, in large part a result of endemic post-communist reliance on foreign investment.

Magyar's victory signals the start of a new geopolitical fiscal regime for Hungary, with hopes that relaxing windfall taxes on banks and removing vetoes on EU funding for Ukraine will unlock the roughly €20bn in support grants and loans that have been frozen in Brussels (amounting to roughly 10 per cent of the national GDP).

Magyar has made a great many contradictory manifesto pledges, however, with promises of lowering taxes, investing $1.5bn in state infrastructure, and cutting the deficit, all while maintaining a ‘pragmatic’ relationship with both Russia and the EU. This begs the question as to whether Magyar – indebted to a Fidesz pedigree himself – represents a break in continuity at all, or just a shift in emphasis of the Fideszian post-Communist political baseline of the Hungarian political class. To what extent Hungarian sovereignty can survive the tumults of contemporary Europe is yet to be seen, but Western capital will certainly be expecting a much simpler route into the country’s national assets than before.

Despite the fall of one ‘sovereigntist’ leader, the spectre of sovereignty remains; as global profit rates continue to fall, the anxious desire for greater national control against volatility is shaking continental markets. The British government is banking on a neo-physiocratic regime, wherein the state no longer manages growth but merely rations declining profits to protect the solvency of credit markets. From Miliband’s SMR contracts to Kendall’s ‘Sovereign AI’, ‘sovereignty’ is being fought for under a single strategy: the nationalisation of risk plus the renting out utility.

Where the AI ‘miracle’ offers a $2trn depreciative sink for excess capital, the material reality remains dictated by the physical. The example set in the Strait of Hormuz and the strike mandate mustered at Ofgem both represent a sovereignty decided by the exception, by the power to withdraw from and, if needed, stop the global machinery. While Hungary appears to trade autonomy for EU credit, and the UK tries to leverage that credit for itself, the class struggle for true sovereignty carries on.